Online checkouts often ask for a card verification code (CVC), but what it actually proves in fraud prevention is easy to miss.

A CVC is a short security code printed on your card that helps confirm you have the card during certain payments.

This article explains what the code checks, where to find it, and how modern security reduces reliance on static code, so you can enter details safely and spot unusual requests.

Key Takeaways

CVC checks help confirm that a buyer likely has access to the card details during online and phone payments, but they do not prove identity or guarantee a legitimate purchase.

The security code may be called CVC, CVV, or CID, depending on the card network, but it serves the same purpose and is checked during card-not-present transactions.

Merchants are prohibited by PCI rules from storing the printed security code after authorization, and modern tools like tokenization and digital wallets reduce how often static card details need to be shared.

What Is the CVC on a Card?

The CVC is a card security code used as an extra verification input for some purchases, especially when the card is not physically read.

It is separate from the card number, which identifies the account, and separate from a PIN, which is used for some in-person debit transactions.

When a merchant sends an authorization, the issuer can return a match or a mismatch result for the submitted code. That result is one signal among many, so a correct code does not guarantee a legitimate purchase.

What the CVC Proves in a Transaction

A correct CVC mainly suggests the payer had access to the security code on the card, which supports a basic possession check. It does not prove identity, because a card can be lost, shared, or photographed.

Payment systems often combine this check with other risk signals, such as transaction patterns and device data.

CVC vs Card Number: How They Work Together

The card number is the primary account number, used to route the payment.

The CVC is a separate value treated as sensitive authentication data under PCI guidance.

In simple terms, the card number identifies which account to charge, while the CVC helps assess whether the buyer likely has the card details.

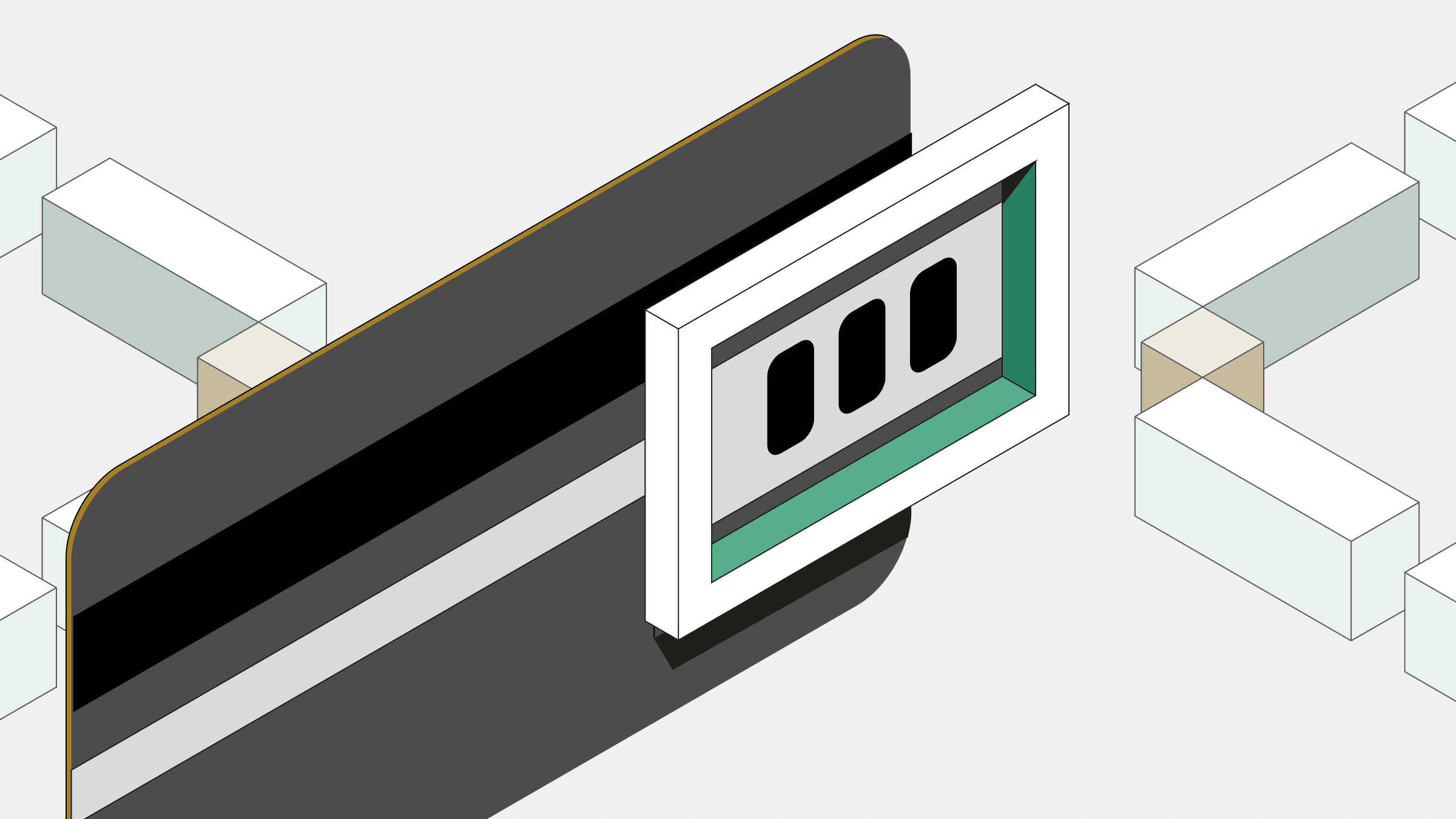

Where to Find the CVC on Your Card

CVC Location on Different Card Types

On Visa and Mastercard, the code is typically the three digits in the signature panel area. On American Express, the code is typically four digits printed on the front above the account number.

Some card designs vary slightly, but most cards use the format mentioned above, so it’s important to use the network pattern as your reference.

Why CVC Codes Have Different Formats

The format varies by card network, so the expected code length depends on whether you are using Visa, Mastercard, or American Express. Card networks set their own specifications for these security codes, so the length and placement are not universal.

If a checkout rejects your code, it can be due to a format mismatch or an incorrect entry. Confirm you used the correct side of the card and the expected digit count for your network.

CVC, CVV, and CID: What’s the Difference?

How Each Network Uses a Different Term

Card networks use different names for the same type of security code. CVC stands for Card Verification Code and is commonly associated with Mastercard, while CVV stands for Card Verification Value and is often used as a general or Visa-related term.

CID stands for Card Identification Number and is used by American Express for the security code printed on the front of the card. Although the names differ, each term refers to a short code used to help verify certain payments.

Some systems and regions also use labels such as CSC, meaning Card Security Code, or CVN, reflecting older or regional terminology, as listed by Sycurio. To avoid brand-specific wording, many merchants simply label the field as a security code.

Do They Function the Same Way?

In most cases, the code is submitted during authorization and checked by the issuer, which can return a match indicator. In some situations, the check may be skipped or handled differently due to merchant settings, network rules, or alternative security methods.

For consumers, the main visible difference remains where the code appears on the card and whether it is three or four digits, even though the underlying checks can vary by payment flow and security setup.

How the CVC Works in Online and Phone Transactions

Card-Not-Present (CNP) Transactions Explained

A card-not-present transaction is one where the card is not physically presented to the merchant at purchase time. CVC checks are common in card-not-present situations, such as e-commerce and mail or telephone orders.

In these flows, the merchant cannot read chip or contactless data, so the buyer types or speaks the details. Because details are entered remotely, criminals may target these flows using stolen data. That is why merchants and issuers use layered checks beyond just the printed code.

How the CVC Verifies Ownership in Digital Payments

When you enter the code, the merchant submits it and receives a response indicating whether it matched issuer records.

A match suggests the buyer likely had access to the printed code on the card. Separately, PCI rules prohibit merchants from storing the printed code after authorization.

A mismatch can raise risk signals, but it can also be caused by a typing error or using the wrong digits.

What Happens When the CVC Is Incorrect

Some merchants decline immediately after a mismatch, while others ask you to re-enter the code. Repeated failures can also trigger issuer controls, depending on the account and merchant.

If you are confident you typed correctly, you should check whether the form expects a three-digit or four-digit value.

Why Merchants Can’t Store CVC Codes

PCI DSS Compliance and Security Standards

PCI DSS stands for the Payment Card Industry Data Security Standard, which is a set of requirements for organizations that store, process, or transmit card data, as outlined by the PCI Security Standards Council.

The PCI quick guide states sensitive authentication data must never be stored after authorization, including the printed security code. That rule applies even if a customer gives permission.

These restrictions reduce how often the most reusable payment inputs can be recovered from a merchant system.

How CVC Protection Limits Data Breach Risks

If a database leaks only a card number and expiry date, it can still be misused, but it may be less useful in some CNP checks.

Keeping the printed code out of storage reduces the chance that a breach exposes the full set of remote payment inputs. This aligns with the broader PCI approach of limiting stored sensitive authentication data.

Beyond CVC: Advanced Card Security Technologies

Dynamic CVC Codes and How They Work

Some issuers use a dynamic code that changes over time instead of a static printed value. The benefit is that a captured code can become stale faster, reducing certain reuse patterns. It’s also important to note that availability can vary by issuer and region.

The Role of Tokenization and Encryption

In card payments, tokenization means replacing the real card number with a substitute value, called a token, that can be used for payment but has no value if stolen. The token cannot be reversed into the original card number outside controlled systems.

For example, when you save a card with a merchant or pay using a digital wallet, the merchant may store a token instead of your actual card number. If that system is breached, the exposed token cannot be reused to make payments elsewhere.

Encryption protects card data while it is moving between systems, so intercepted traffic is unreadable without the proper keys. Together, tokenization and encryption reduce how often a static security code is the only line of defense.

How Digital Wallets Improve Payment Security

Digital wallets commonly use tokens, so the merchant receives a token, not the original card number. Apple says Apple Pay uses a device-specific account number and a dynamic security code for each transaction.

Wallets typically require device authentication, such as biometrics or a passcode, before authorizing a payment, although some transit payments can use Express Mode where available.

What to Do If Your CVC Is Damaged or Illegible

When to Request a New Card

Request a new card if the code is illegible and you regularly make remote purchases that require it.

Consider replacement sooner if you suspect the card was copied or photographed without permission.

If fraud is suspected, contact your issuer as soon as possible through official channels.

Why CVC Codes Can’t Be Retrieved or Reissued

Because the code is not supposed to be stored by merchants after authorization due to PCI rules, systems are not designed for a merchant to look it up.

Issuers can issue a new card, but they generally do not reveal the existing code through customer service chat logs or email.

That design keeps the code tied to physical possession.

How to Keep Your Card and CVC Secure

Safe Practices for Online Purchases

Simple habits can significantly reduce the risk of your card details being captured during online payments, especially in card-not-present transactions. Here are a few habits that could help:

Type card details only on sites you reached deliberately, not from unexpected messages.

Prefer checkout methods you recognize, including wallets, especially on shared devices.

Keep your browser and phone updated to reduce exposure to malware and exploit-based attacks that can follow phishing attempts.

Avoiding Phishing and Data Theft

Treat the CVC like a purchase secret, and share it only when you are intentionally paying a trusted merchant. Avoid making mistakes like sending the full set of card details over email or messaging apps.

Be cautious with links, pop-ups, and phone calls that request card details without a clear purchase context.

Monitoring Card Activity for Fraud

Review transactions regularly so you can spot unfamiliar purchases quickly.

Turn on account alerts if your bank offers them, especially for online transactions.

If you see an unrecognized charge, contact your issuer immediately and follow its dispute process.

Final Thoughts: The Last Line of Defense in Card Security

It helps to think of the CVC as a small but important final check in many remote purchases. When you enter it, you are adding a possession signal that can make stolen card details harder to use on their own.

That safeguard works partly because the code is not meant to live in merchant systems. PCI guidance treats the CVC as sensitive authentication data and prohibits storing it after authorization, which limits how often it can be recovered in a breach.

Many modern payment experiences reduce reliance on static card details altogether. Tokenization and wallet payments can limit exposure of card credentials by using payment tokens in place of the card number in many merchant flows.