Stablecoins can move value across borders in seconds, but most day-to-day commerce still runs through card networks, bank transfers, and cash. The gap between holding digital dollars and actually spending them at a checkout terminal is a practical infrastructure problem.

Card issuance is the technical and regulatory layer that bridges this gap. It allows digital wallets to convert stablecoin balances into payment cards accepted at millions of physical and online merchants, without requiring the merchant to change anything about how they operate.

This article explains how card issuance works, what changes when stablecoins replace traditional bank accounts as the funding source, and how issuance platforms like Rain connect onchain balances to card network rails.

Key Takeaways

Stablecoin-backed cards maintain a standard merchant experience while using digital assets for funding and issuer-side settlement.

Card issuance involves complex compliance, fraud monitoring, and dispute management beyond generating card numbers.

Stablecoins can change the issuer-side plumbing (funding, settlement, treasury) while the merchant and cardholder experience stays the same.

Rain provides the card issuance infrastructure that connects Plasma One's consumer and business banking platform to global card networks.

What Card Issuance Actually Involves

Card issuance is the process of creating and managing payment cards, including the underlying accounts, spending limits, and authorization logic that determines whether a transaction gets approved or declined. It is the bridge between a user’s store of value and the global payment ecosystem managed by networks like Visa and Mastercard.

Beyond the physical or virtual card itself, issuance covers essential operational workflows: processing disputes, managing chargebacks, handling refunds, monitoring for fraud, and maintaining compliance with financial regulations. These back-office functions ensure that both the cardholder and merchant can resolve transaction errors through established frameworks.

Building this infrastructure from scratch is capital-intensive and highly regulated. Most teams rely on an issuance platform that provides the necessary infrastructure to connect digital balances to card network rails without requiring the developer to become a licensed financial institution.

The Key Roles in a Card Payment

A card payment involves four main parties, each with a distinct role:

The cardholder initiates the purchase by presenting their card (physical tap, mobile wallet, or online checkout). This triggers an electronic authorization request that must be validated against a balance or credit line held within the issuer’s system.

The merchant accepts the card through an acquiring bank (the bank that processes card payments on behalf of the merchant). The merchant is indifferent to the cardholder’s underlying asset. They receive fiat settlement in their chosen currency via their acquirer, subject to standard fees and chargeback rules.

The card network (Visa, Mastercard) provides the communication rails that route authorization and settlement messages between the acquirer and issuer. This network ensures that a transaction initiated in one country can be verified by an issuer in another within seconds.

The issuer makes the final decision to approve or decline based on available funds and risk checks. Once approved, the issuer is responsible for settling with the merchant’s side through the card network’s standard settlement process.

A detailed walkthrough of the traditional card payment authorization flow, showing how transactions move from the cardholder and merchant through acquirers, card networks, and issuing banks before approval and settlement. Source: Toucan

The Problem Card Issuance Solves for Stablecoins

Merchants rarely accept stablecoins directly at checkout. There are technical integration barriers, accounting complications, and most merchants have no reason to change their existing payment acceptance infrastructure. This creates a utility gap: users hold digital dollars but cannot spend them for everyday purchases.

Card issuance bridges this gap by converting a wallet balance into a format that the merchant’s terminal already understands. The user spends their stablecoins; the merchant receives their local fiat currency as usual. Neither party needs to change their behavior.

Where Stablecoins Fit in the Card Stack

In a traditional card program, the user’s funds sit in a fiat bank account, and the issuer settles with the card network through standard banking rails (wires, ACH). Stablecoins can replace one or both of these layers.

The Funding Model

In the funding model, the user holds stablecoins in a wallet or dedicated program account. When a transaction occurs, the system checks this onchain or ledger-based balance to ensure the user has sufficient funds.

The program places a hold at authorization and finalizes the debit at clearing. This gives the user a familiar card experience while their balance remains denominated in stablecoins. From the cardholder’s perspective, the experience is identical to a traditional prepaid or debit card.

The Settlement Model

Authorization happens in seconds, but card network settlement (the actual movement of money from the issuer to the merchant’s bank) follows its own timelines, typically T+1 or T+2. In a traditional program, this settlement happens via banking rails restricted to business hours.

When the issuer side uses stablecoins for settlement and treasury management, it can operate outside banking hours. Stablecoins settle rapidly and daily, which means treasury teams can rebalance liquidity and fund settlement obligations without waiting for bank cutoffs. This can reduce reliance on international wires for some settlement flows.

What Changes and What Stays the Same

The critical point is that stablecoins change the issuer-side plumbing while the merchant experience stays identical. The merchant never sees stablecoins. They receive fiat via the card network’s standard settlement process, exactly as they would with any other card program.

How a Stablecoin Card Transaction Works

The Authorization Flow

When a cardholder taps their card at a terminal or enters their details for an online purchase, the following sequence occurs:

The merchant’s acquiring bank sends an authorization request to the card network.

The card network routes the request to the issuer stack (operated by the issuance platform or program manager).

The issuer stack verifies the cardholder’s identity, runs risk and fraud checks, and checks whether the stablecoin-linked account has a sufficient balance.

If approved, a response travels back through the network to the merchant’s terminal within seconds.

The program ledger records the hold, and the user typically receives an instant notification.

This flow is identical to a traditional card transaction. The only difference is that the balance check happens against a stablecoin-denominated account rather than a fiat bank account.

Settlement Happens After Authorization

It is important to understand that settlement and authorization are separate events. While the merchant sees approval instantly, the actual transfer of funds from the issuer to the merchant’s bank follows the card network’s settlement schedule, typically one or more business days later.

When issuers use stablecoins for their treasury and settlement processes, they can fund settlement obligations around the clock rather than being constrained by banking hours. This operational flexibility is one of the key advantages of stablecoin-backed card programs for issuers and program managers.

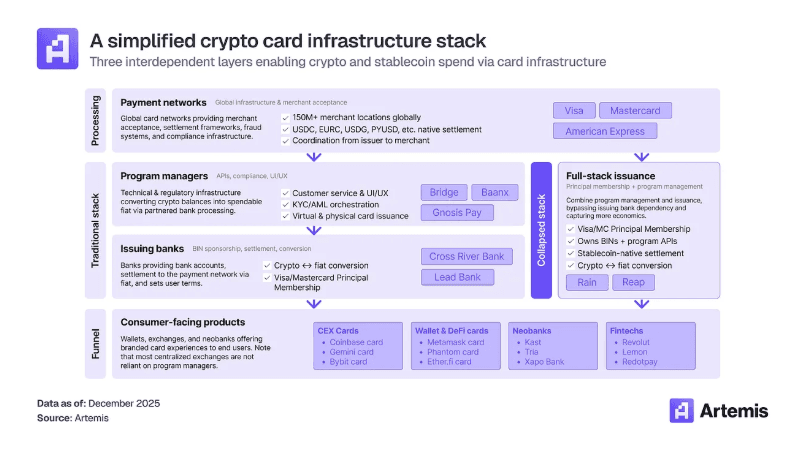

Layered diagram of the crypto card infrastructure stack, showing payment networks, program managers, issuing banks, and consumer crypto card products. Source: Artemis

Traditional vs. Stablecoin-Powered Card Programs

Feature | Traditional Card Program | Stablecoin-Powered Card Program |

|---|---|---|

Funding Source | Fiat bank account (USD, EUR, etc.) | Onchain stablecoins (USD₮, USDC) |

Settlement Rail | Legacy wires / ACH | Stablecoins or fiat rails |

Merchant Experience | Receives fiat via card network | Receives fiat via card network |

Operational Hours | Restricted by banking hours | Rapid and daily treasury potential |

Rain on Plasma: How It Works in Practice

Rain is a stablecoin-native payments infrastructure provider that helps enterprises and fintechs issue cards, move money, and make digital dollars spendable in the real world.

Rain's integration with Plasma One is one example of how stablecoin balances can be connected to card-based spending without changing the merchant experience. Rain provides the card issuance layer, while Plasma One is the consumer and business banking platform where members hold and manage their USD₮.

Rain’s Role: Issuance Infrastructure

Rain is the card issuer and a Visa Principal Member. Rain handles card program setup, compliance workflows, authorization logic, and the ledger system that links a stablecoin-funded account to a card transaction. Rain also manages dispute processing, chargeback handling, and the regulatory requirements associated with card issuance.

Rain has discussed using stablecoins for Visa settlement as part of broader stablecoin settlement efforts.

Plasma’s Role: Consumer and Business Banking

Plasma One is a consumer and business banking platform where members hold, send, and spend USD₮. The platform is built on infrastructure designed for fast stablecoin movement and offers fee-free USD₮ transfers for eligible transactions. This means frequent top-ups and internal funding flows happen without extra costs or friction for members.

The End-to-End Flow

In practice, the flow works like this:

A Plasma One user funds their account with USD₮.

After a thorough KYC process, Rain provisions the card and applies spend controls and compliance checks.

The user spends anywhere the card network is accepted.

The program reconciles card-ledger movements with onchain balances to keep accounting and user visibility aligned.

From the user’s perspective, this feels like a standard fintech card. They hold a balance, they spend it, they get notifications. The stablecoin infrastructure is invisible.

Rain and Plasma make stablecoins feel like money. Rain

Why Stablecoin-Native Rails Matter for Card Programs

Everyday card spending creates high-frequency ledger activity. Every authorization, hold, clearing, and settlement event needs to be tracked and reconciled. Stablecoin-native rails can reduce friction in several of these flows.

Fast finality means that funding events (user tops up their card balance) settle quickly rather than waiting for ACH or wire processing windows. Low transfer overhead means treasury teams can rebalance liquidity more frequently without incurring high per-transaction costs.

Some networks, including Plasma, support fee sponsorship for simple stablecoin transfers, so users do not need to hold a separate gas token just to fund a card account. This design decision removes a significant friction point that would otherwise make the experience feel distinctly "crypto" rather than fintech.

Connecting Onchain Balances to Real-World Spending

Stablecoins make digital dollars easy to move at the speed of the internet. Card issuance makes them spendable at the point of sale. The combination connects the efficiency of onchain settlement with the universal acceptance of card networks.

Plasma builds consumer and business financial products with stablecoins at the core. It's flagship consumer neobank is Plasma One. Every layer of the stack is built so that spending, saving, and moving money works the way people expect: instant, predictable, secure, and simple.

As stablecoin-backed card programs mature, the distinction between "crypto card" and "regular card" will continue to fade. The underlying asset changes, but the payment experience stays the same.

Disclaimer

This article is for educational and informational purposes only. It does not constitute, and should not be construed as, investment advice, financial advice, legal advice, tax advice, a solicitation, an offer, or a recommendation to buy, sell, or hold any digital asset or financial instrument. Card programs described are subject to eligibility requirements, geographic restrictions, and regulatory approvals. Card issuance and program management are provided by Rain, not by Plasma. Stablecoin products and services may not be available or lawful in all jurisdictions. Readers should conduct their own due diligence and consult qualified professionals before making any decisions.