Stablecoin vs. High-Yield Savings Accounts: Which Earns More?

Stablecoin transaction volume averaged $1.5-2.0 trillion USD per month in early 2024, significantly surpassing traditional wire transfers in speed and cost-efficiency.

Stablecoins are cryptocurrencies pegged to fiat currencies like the US dollar that generate yield through DeFi lending protocols and centralized platforms, offering 3-6% APY with instant global settlement, while high-yield savings accounts provide FDIC-insured returns of 4.5-5.35% APY with regulatory certainty but slower transaction times and geographic restrictions.

You will learn how these two savings vehicles compare across yield potential, transaction efficiency, risk profiles, and optimal use cases, equipping you with a framework to allocate capital based on your risk tolerance and financial objectives.

Key Takeaways

Stablecoins deliver superior transaction speed and lower costs for cross-border payments alongside competitive yield potential, but carry smart contract, de-peg, and counterparty risks that require active management

High-Yield Savings Accounts provide unmatched principal safety through $250,000 FDIC insurance, regulatory clarity, and operational simplicity, making them ideal for emergency funds and conservative investors

The optimal strategy typically involves a hybrid approach, balancing the security of HYSAs for core reserves with diversified stablecoin holdings for enhanced yield and global accessibility

Understanding Stablecoins: Yield, Features, and Risks

Stablecoins maintain price stability by pegging to fiat currencies while generating yield through multiple mechanisms, creating an asset class that bridges traditional finance and digital infrastructure. Unlike volatile cryptocurrencies, their design prioritizes predictable value preservation while enabling participation in higher-yield opportunities unavailable through conventional banking channels.

How Stablecoins Generate Yield

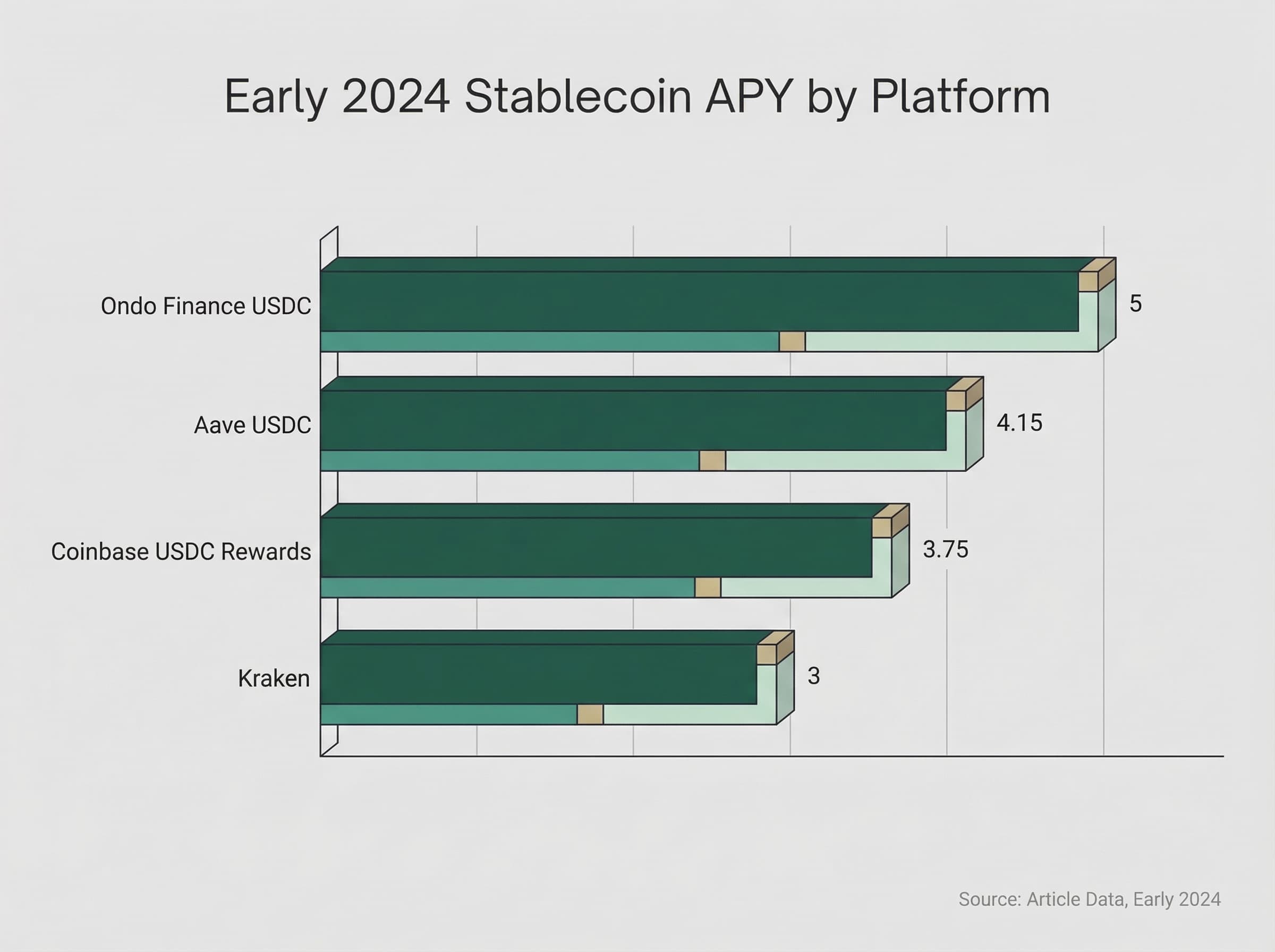

DeFi lending protocols represent the primary yield generation mechanism for stablecoins. Platforms like Aave and Compound allow users to deposit assets into smart contract-based lending pools where borrowers pay interest to access liquidity. Aave offered 3.2-5.1% APY on USDC deposits during early 2024, with rates fluctuating based on supply and demand dynamics. The smart contracts execute automatically via blockchain consensus, eliminating intermediaries and enabling real-time yield accrual with continuous compounding.

Centralized platforms provide a more accessible entry point for yield generation, requiring only standard account creation rather than blockchain wallet management. Coinbase USDC Rewards delivered 3.5-4.0% APY in early 2024, while Kraken offered 2.5-3.5% APY through tiered staking programs. These platforms custody user assets and distribute yields through traditional account structures, reducing technical barriers while introducing counterparty risk.

Treasury-backed stablecoin products emerged as conservative alternatives that blend blockchain efficiency with traditional asset backing. Ondo Finance offered 4.8-5.2% APY on USDC in February 2024 by allocating reserves to short-term US Treasury Bills, providing institutional-grade risk management while maintaining stablecoin liquidity advantages. This model appeals to risk-conscious investors seeking blockchain benefits without exposure to volatile DeFi protocols.

Key Features and Benefits of Stablecoins

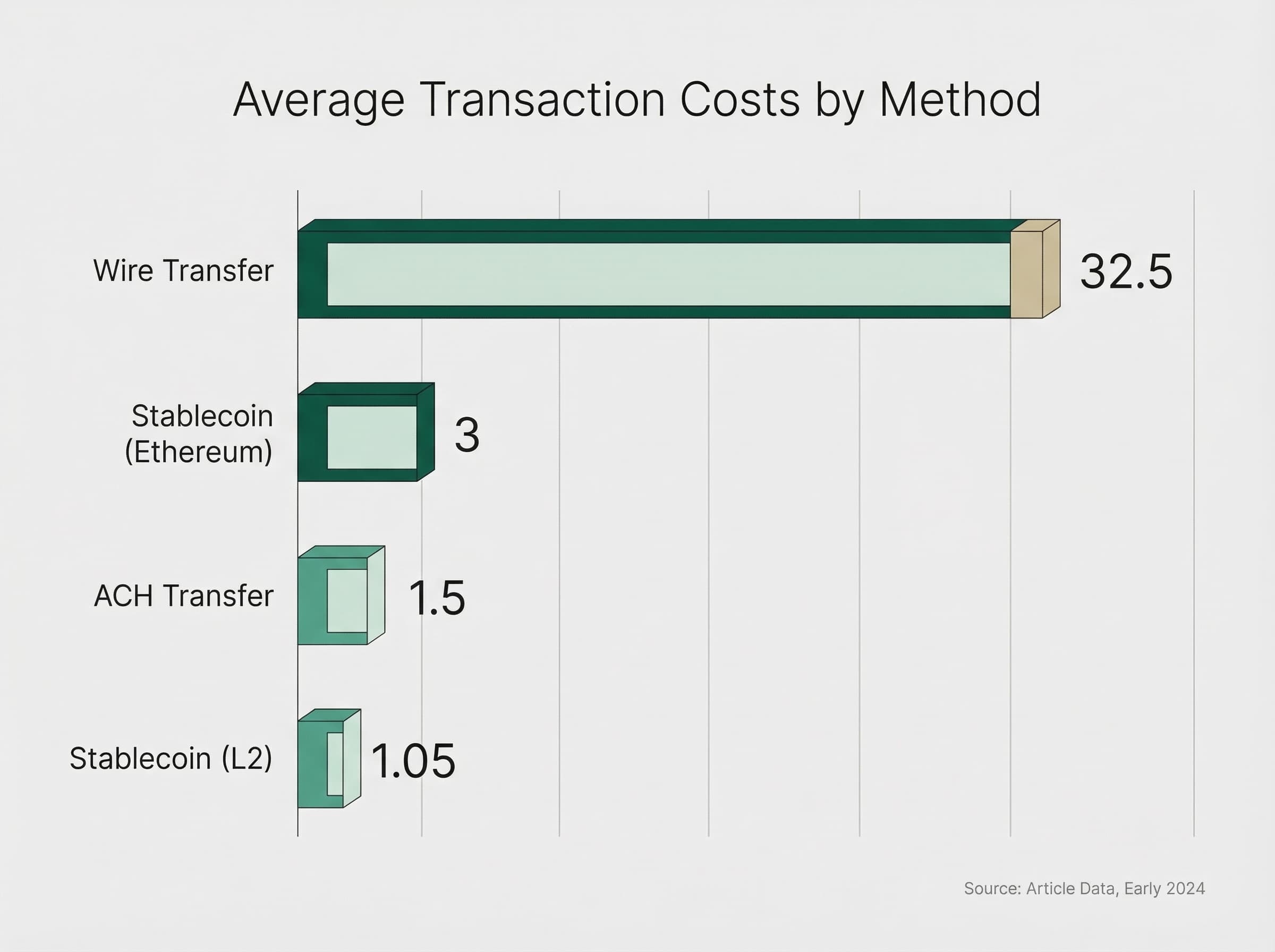

Global accessibility defines the core value proposition of stablecoins, operating 24/7 without banking hours or geographic restrictions. Settlement occurs in under one minute on Ethereum mainnet and under 15 seconds on Layer 2 networks like Polygon and Arbitrum, compared to 1-3 business days for ACH transfers. Transaction costs range from $0.10-$5 regardless of transfer amount, representing a 60-98% cost reduction versus $15-50 wire transfer fees for comparable transactions.

The $1.5-2.0 trillion in monthly stablecoin transaction volume recorded in early 2024 reflects widespread adoption across remittance corridors, business treasury management, and trading operations. This infrastructure enables instant cross-border settlement without correspondent banking delays, particularly valuable for businesses managing multi-currency operations or individuals in countries with restrictive banking systems. The 1.7 billion unbanked adults globally can access these services with only a smartphone and internet connection.

Higher yield potential remains compelling despite recent compression from 2022 peaks. While early 2024 stablecoin yields of 4-8% across centralized and DeFi platforms converged with HYSA rates of 4.5-5.35%, stablecoins maintain advantages in programmability and composability. Smart contract integration enables automated recurring payments, conditional transfers, and sophisticated treasury workflows impossible within traditional banking infrastructure.

Understanding Stablecoin Risks

De-peg risk represents the most visible failure mode for stablecoins, occurring when market forces or structural vulnerabilities break the dollar peg. UST collapsed in May 2022 after its algorithmic mechanism failed, losing 99% of value within days. Even fully-backed stablecoins face temporary de-peg scenarios, as demonstrated when USDC briefly traded at $0.88 during the March 2023 Silicon Valley Bank collapse before recovering within 48 hours as reserves were clarified.

Mitigation requires selecting stablecoins with transparent reserve attestations and overcollateralized backing. USDC and USD₮ maintain reserves exceeding circulating supply, published through monthly third-party audits. Avoiding algorithmic designs entirely eliminates the most catastrophic risk category, while diversifying across multiple stablecoins prevents single-point-of-failure exposure during isolated de-peg events.

Smart contract vulnerabilities create permanent loss scenarios that no insurance covers. The 2023 Curve Finance exploit resulted in $570,000 in losses when protocol code contained unexpected interactions. Audited protocols like Aave and Compound undergo multiple third-party security reviews, but audits cannot guarantee absolute safety. Starting with small deposits, verifying audit reports directly, and monitoring protocol Total Value Locked as a proxy for institutional confidence reduces but cannot eliminate this risk.

Counterparty risk in centralized platforms became acute during 2022-2023 liquidity crises. Celsius filed Chapter 11 bankruptcy in 2022 while BlockFi faced insolvency, freezing customer deposits worth billions. Genesis Global Capital encountered similar liquidity issues in 2023 during market volatility. Institutional-grade custodians like Coinbase Custody and Kraken Custody provide greater operational transparency and regulatory oversight, while self-custody through hardware wallets eliminates counterparty exposure entirely at the cost of increased operational responsibility.

Regulatory uncertainty persists despite emerging frameworks. The European Union's MiCA regulation establishes comprehensive stablecoin standards by end of 2024, while US regulatory approaches remain fragmented across SEC, CFTC, and OCC jurisdictions. This uncertainty creates jurisdictional arbitrage opportunities but also introduces risks of sudden policy changes that could restrict access or impose capital controls on stablecoin holdings.

High-Yield Savings Accounts: Safety, Simplicity, and Limitations

High-Yield Savings Accounts represent the cornerstone of conservative financial planning, offering above-market interest rates within the traditional banking system's regulatory framework. These accounts combine federal deposit insurance with operational simplicity, providing absolute principal protection at the expense of transaction flexibility and yield optimization.

The Core Appeal: FDIC Insurance and Simplicity

The Federal Deposit Insurance Corporation guarantees deposits up to $250,000 per depositor per institution, backed by the full faith and credit of the US government. This protection eliminates principal risk from bank failures, operating through multi-tiered regulatory oversight involving the Federal Reserve, Office of the Comptroller of the Currency, and state banking regulators. Banks must maintain reserve ratios, undergo stress testing, and comply with liquidity requirements that create systemic stability absent from cryptocurrency platforms.

Operational simplicity attracts users uncomfortable with blockchain technology or unwilling to manage private keys. Account setup requires only standard identification, with familiar interfaces mirroring checking account functionality. Direct deposit integration, physical branch access at many institutions, and decades of brand recognition create trust that newer digital alternatives cannot replicate. The straightforward tax treatment through 1099-INT reporting and clear legal framework under Regulation E and TILA-RESPA provide additional certainty for conservative investors.

Yield Generation and Rates

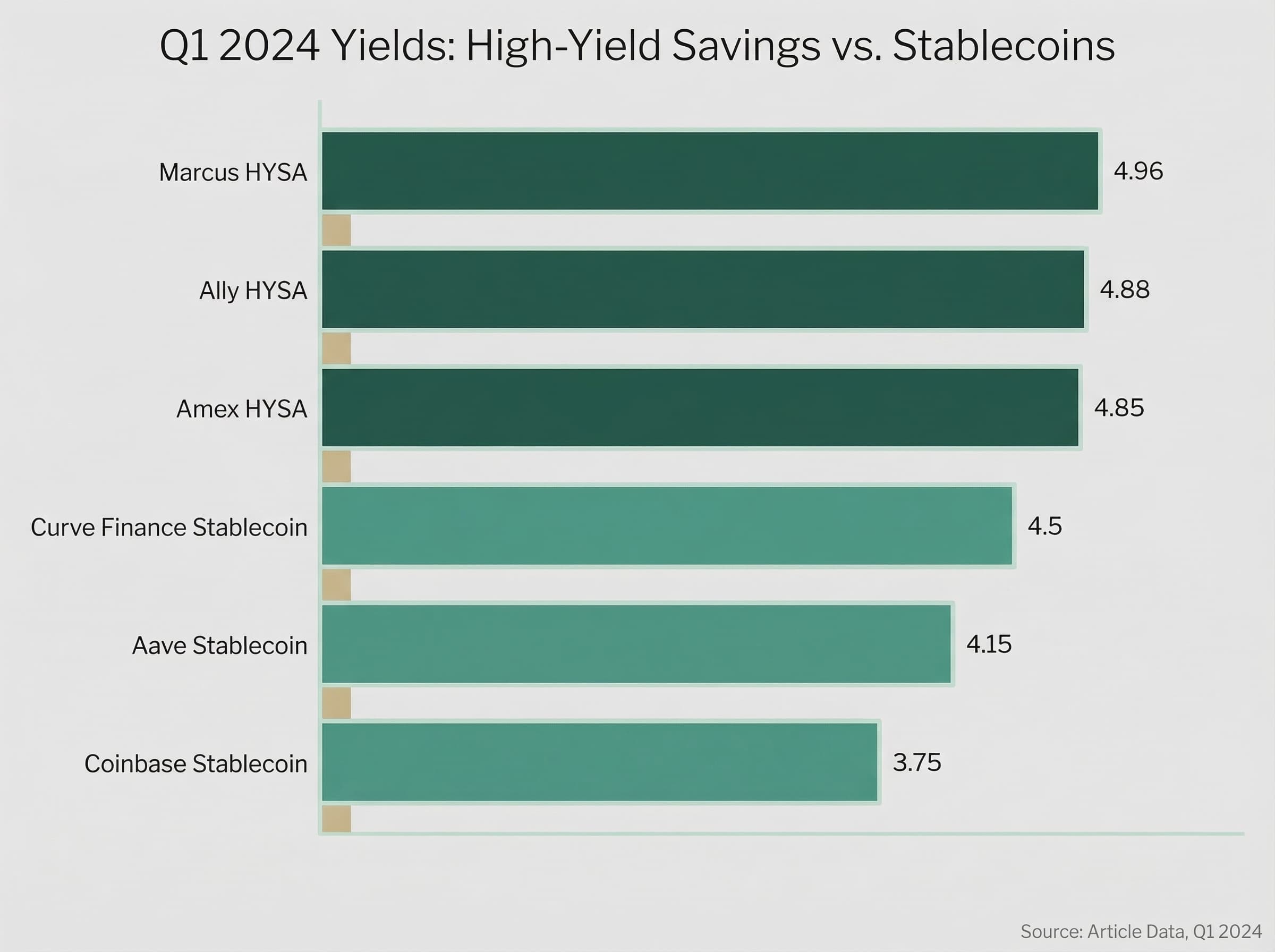

Interest rates on HYSAs track Federal Reserve policy decisions, increasing sharply during the 2022-2023 tightening cycle. Marcus by Goldman Sachs offered 4.96% APY in Q1 2024, while Ally Bank provided 4.88% and American Express Personal Savings delivered 4.85%. These rates represent a 500+ basis point increase from December 2021, when online HYSAs averaged 0.35% APY before the Fed began raising rates from near-zero levels.

The lag between Federal Funds Rate adjustments and HYSA rate changes reflects bank margin requirements. With the Fed Funds Rate at 5.25-5.33% in March 2024, HYSAs typically trail by 25-50 basis points as banks balance competitive positioning against profitability targets. This structural lag means HYSA rates compress both when rates rise and when they fall, creating asymmetric responsiveness that favors banks over depositors during rate transitions.

Limitations and Risks of HYSAs

Inflation erosion represents the primary risk to HYSA purchasing power, particularly during high-inflation periods when nominal yields fail to keep pace with consumer price increases. With CPI inflation at 3.2-3.4% in Q1 2024 and HYSA yields at 4.85%, real returns reached only 1.65%. This modest positive return contrasts sharply with 2022, when 8.0% inflation overwhelmed 1.2% average HYSA yields to produce a devastating -6.8% real return that significantly eroded purchasing power.

Transaction inefficiencies compound when moving money across borders or accessing funds outside business hours. ACH transfers require 2-3 business days for settlement at costs of $0-3, while international wire transfers cost $25-50 and take 3-5 business days through correspondent banking networks. Same-day domestic wires are available but add $15-50 in fees, making rapid access expensive compared to instant stablecoin settlement.

Geographic and operational restrictions limit flexibility for modern financial workflows. Many institutions retain monthly withdrawal limits of 6 transactions despite Federal Reserve rule changes in 2020. Minimum balance requirements ranging from $0-25,000 across institutions create barriers to entry, while monthly service fees of $5-15 apply when balances drop below thresholds. Support operates primarily during business hours, with limited international accessibility for some regional banks serving domestic markets exclusively.

Stablecoins vs. HYSAs: A Quantitative and Qualitative Comparison

The convergence of stablecoin and HYSA yields in 2024 masks fundamental differences in accessibility, transaction efficiency, and risk architecture. While nominal returns now overlap in the 4-6% APY range, the operational characteristics and security models diverge sharply, creating distinct use cases that align with different financial priorities and risk tolerances.

Yield Potential and Real Returns

Q1 2024 data reveals substantial yield compression across both asset classes. HYSAs averaged 4.5-5.35% APY, with Marcus at 4.96%, Ally at 4.88%, and American Express at 4.85%. Stablecoins delivered 3.5-6.0% APY depending on platform selection, with Coinbase USDC Rewards at 3.5-4.0%, Aave USDC deposits at 3.2-5.1%, and Curve Finance pools at 3-6%. The historical arbitrage that favored stablecoins during 2022 peaks of 8-15% APY has normalized as DeFi yields responded to broader interest rate environments and risk-adjusted return expectations.

Inflation impact determines whether nominal yields translate to purchasing power preservation. With US CPI inflation at 3.2% year-over-year in Q1 2024, the 4.85% average HYSA yield produced a 1.65% real return, while stablecoin yields of 4.5% generated approximately 1.3% real returns. These modest positive real returns represent significant improvement from 2022, when 8.0% inflation created -6.8% real returns for HYSAs and -2% to 0% for stablecoins. A $100,000 deposit lost $6,800 in purchasing power through an HYSA during 2022, compared to $0-2,000 through stablecoins.

The 500+ basis point increase in HYSA rates from December 2021 through March 2024 demonstrates traditional banking's responsiveness to Federal Reserve policy, while stablecoin yield volatility reflects the speculative cycles and protocol maturation within DeFi markets. Stablecoin yields peaked during excessive leverage periods and crashed following Terra/Luna collapse in May 2022, stabilizing thereafter as risk management improved and speculative capital exited the ecosystem.

Transaction Efficiency and Accessibility

Transaction metrics reveal stablecoins' overwhelming advantages for cross-border payments and rapid settlement. Layer 2 networks process stablecoin transfers for $0.10-2.00 with settlement under 15 seconds, while Ethereum mainnet requires $1-5 in gas fees with finality achieved in under one minute. Wire transfers cost $15-50 and settle in 1-3 business days domestically or 3-5 days internationally, while ACH transfers take 2-3 days at $0-3 cost.

For a $10,000 cross-border transfer, stablecoins reduce costs by 60-98% compared to wire transfers, saving $23-48 per transaction while delivering 99.9% faster settlement. These efficiency gains compound for businesses managing high transaction volumes or individuals in remittance corridors. El Salvador documented 67% year-over-year growth in cryptocurrency and stablecoin remittance volumes in 2022, driven by cost savings of $276-288 annually for workers sending $500 monthly versus traditional 5% remittance fees through Western Union.

The 1.7 billion unbanked adults globally lack access to traditional banking infrastructure, making HYSAs unavailable regardless of their advantages. Stablecoins require only smartphone access and internet connectivity, enabling financial inclusion in regions with weak banking infrastructure or capital controls. This accessibility extends to 24/7 operation without holidays or banking hours, providing liquidity flexibility impossible within traditional systems operating on business day schedules.

Risk Profiles and Regulatory Landscape

FDIC insurance provides absolute principal protection up to $250,000 per depositor per institution, eliminating bank failure risk through governmental guarantee backed by regulatory oversight and deposit insurance funding. This guarantee contrasts sharply with stablecoin exposure to smart contract vulnerabilities, de-peg events during stress scenarios, and counterparty risk from platform insolvency. USDC's brief $0.88 de-peg during Silicon Valley Bank's March 2023 collapse demonstrated that even fully-backed stablecoins face temporary volatility during systemic banking stress.

Regulatory perspectives highlight divergent institutional views on stablecoin viability. Jerome Powell testified to Congress in February 2023 that stablecoins raise concerns about financial stability and require comprehensive regulatory frameworks including prudential standards and capital requirements. SEC Chair Gary Gensler emphasized in March 2023 that significant risks persist until proper regulation establishes consumer protections. Former FDIC Chair Sheila Bair argued in 2023 that stablecoins could complement banking but cannot replace deposit insurance protections.

Counter-perspectives from stablecoin advocates emphasize transformative potential. Jeremy Allaire, CEO of Circle, stated in March 2024 that stablecoins are becoming critical financial infrastructure with regulatory clarity positioning them as viable alternatives to traditional systems. Dante Disparte testified to the US Senate Banking Committee in April 2023 that stablecoins serve 1.2 billion unbanked individuals globally, representing transformative financial inclusion contingent on transparent reserve backing and regulatory certainty. The European Central Bank's October 2023 Financial Stability Review acknowledged stablecoin payment efficiency while noting that MiCA implementation by end of 2024 would establish EU-wide frameworks addressing systemic risk concerns.

Strategic Allocation: When to Choose What

Individual financial circumstances dictate optimal allocation between stablecoins and HYSAs, with most investors benefiting from hybrid strategies that leverage each asset class's distinct advantages. Risk tolerance, liquidity requirements, geographic location, and technical capability create a decision matrix that guides appropriate capital deployment across these complementary vehicles.

Decision Framework: Matching Needs to Features

Risk tolerance assessment determines foundational allocation strategy. Conservative investors with low risk tolerance should maintain 90% HYSA allocation with only 10% in stablecoins for exposure to blockchain infrastructure. This profile suits retirees, individuals unable to tolerate principal loss scenarios, and those prioritizing absolute capital preservation over yield optimization. The FDIC guarantee eliminates downside risk at the expense of operational flexibility and modest yield differentials.

Moderate risk tolerance enables balanced 50/50 allocation, deploying half of capital to HYSAs for emergency fund requirements while directing remaining assets to diversified stablecoin platforms. This approach captures higher stablecoin yields of 4-6% on half the portfolio while maintaining core liquidity through FDIC-insured accounts. Small business owners, remote workers earning cryptocurrency, and individuals comfortable with blockchain technology but unwilling to abandon traditional banking fit this profile.

High risk tolerance with strong technical capability supports 80% stablecoin allocation, maintaining only 20% in HYSAs for regulatory-compliant reserves or immediate fiat liquidity needs. Cryptocurrency-native investors, global traders, and businesses with blockchain-denominated operational needs benefit from concentrated stablecoin positioning that maximizes yield and transaction efficiency while accepting smart contract and counterparty risk through active management.

Liquidity requirements and time horizons further refine allocation decisions. Funds needed within 24 hours require HYSA placement despite lower yields, as stablecoin withdrawal to fiat banking systems can introduce 1-3 day delays during platform processing. Short-term liquidity needs of 2-7 days make stablecoins acceptable through conservative platforms like Coinbase or Kraken, which offer rapid withdrawal processing. Long-term holdings exceeding 6 months optimize for stablecoin yield compounding, where 5-6% returns on DeFi protocols meaningfully outpace 4.85% HYSA yields over multi-year horizons.

Geographic considerations create stark differences in optimal strategy. US-based individuals with purely domestic operations find HYSAs and stablecoins roughly equivalent in accessibility, choosing primarily based on yield and risk tradeoffs. International or multi-country operations make stablecoins substantially superior, eliminating $25-50 wire transfer costs and 3-5 day correspondent banking delays through instant settlement at $0.10-5.00 per transaction. Countries with capital controls, banking instability, or financial sanctions render HYSAs partially or fully inaccessible, making stablecoins the only viable option for wealth preservation and cross-border transactions.

Technical capability determines execution feasibility. Non-technical users prioritize HYSAs due to zero blockchain knowledge requirements and familiar banking interfaces. Basic technical capability enables centralized stablecoin platforms like Coinbase that mirror traditional account structures while introducing cryptocurrency exposure. Advanced users can engage full DeFi strategies including self-custody through hardware wallets, direct protocol interaction, and smart contract-based yield optimization, accepting operational complexity in exchange for maximum yield potential and complete asset control.

Security Best Practices for Stablecoin Holdings

Private key management represents the highest-priority security consideration for non-custodial stablecoin storage. Hardware wallets like Ledger and Trezor store private keys offline, eliminating remote hacking vectors that compromise software wallets. The 12-24 word seed phrase must be stored in secure, redundant locations such as safe deposit boxes or distributed among trusted family members, with annual recovery process testing ensuring accessibility during emergencies. Never sharing seed phrases or private keys prevents social engineering attacks that represent the most common loss vector.

Custodial solutions shift security responsibility to institutional platforms but introduce counterparty risk. Coinbase Custody, Kraken Custody, and Fidelity Digital Assets provide institutional-grade security with insurance coverage typically exceeding $250 million, verified through public disclosures and regulatory filings. Avoiding exchanges without demonstrated security infrastructure or unclear custody arrangements prevents exposure to platform failures like Celsius and BlockFi experienced during 2022-2023.

Smart contract due diligence requires verifying third-party security audits before depositing funds. Protocols like Aave and Compound undergo multiple audits from firms including Consensys Diligence, Trail of Bits, and OpenZeppelin, with audit reports published on protocol websites. Audits older than one year should trigger re-verification as protocol upgrades introduce new code that may contain vulnerabilities. High Total Value Locked exceeding $500 million indicates institutional confidence and resources for ongoing security maintenance, while protocols with 2+ year track records demonstrate operational durability through multiple market cycles.

Platform insurance coverage and regulatory status provide additional security layers. Verify platforms carry hacking insurance or maintain dedicated security funds like Aave's Safety Module. Confirm regulatory compliance or clear regulatory pathways such as MiCA compliance in the EU or adherence to OCC guidance in the US. Reading all terms of service, understanding yield sustainability mechanisms, and testing withdrawal processes with small amounts prevents surprises during stress scenarios when rapid capital access becomes critical.

Concentration limits and counterparty risk management prevent catastrophic single-point failures. Never exceed $250,000 FDIC equivalent exposure at any single platform, spreading stablecoin holdings across 2-3 reputable platforms to diversify operational risk. Conservative allocation maintains 70% on stable platforms like Coinbase or Kraken with 30% on higher-yield DeFi protocols, while moderate approaches split 50/50. Maintaining ability to withdraw 100% within 7 days maximum and avoiding lock-up periods exceeding 6 months preserves liquidity flexibility during market stress or personal financial emergencies.

Conclusion: Navigating Your Financial Future with Confidence

The choice between stablecoins and high-yield savings accounts reflects personal financial priorities rather than objective superiority of either vehicle. HYSAs provide unmatched security through FDIC insurance and operational simplicity for emergency funds and conservative savings, while stablecoins unlock global accessibility, transaction efficiency, and competitive yield for investors comfortable managing digital asset risks. Networks like Plasma are building purpose-built infrastructure for stablecoin payments, combining high-throughput processing with regulatory-ready design that makes digital dollar transactions as reliable as traditional banking. Whether you prioritize the robust security of HYSAs or the dynamic potential of stablecoins on platforms like Plasma, understanding each instrument's distinct risk-return profile enables informed allocation decisions. Evaluate your risk tolerance, liquidity requirements, and financial objectives to construct a balanced strategy that leverages both vehicles' complementary strengths for optimal portfolio outcomes.

Ready to get started with Plasma One? Open your account today.