Moving money globally has traditionally been a slow, opaque process. Sending a wire from Miami to Singapore means routing through multiple intermediary banks, waiting 1-5 business days, and losing visibility into where the funds are at any given moment.

Modern on-ramp and off-ramp infrastructure replaces much of this friction by connecting traditional bank rails to stablecoin settlement. Users deposit fiat into a virtual account, it converts to a stablecoin, and transfers onchain in seconds. The reverse works the same way: stablecoins convert back to fiat and land in a bank account.

This article explains how each layer of that pipeline works, from the banking rails that move fiat, to the virtual account systems that route and reconcile it, to the stablecoin minting process that puts value onchain. It also covers how Bridge’s infrastructure handles these conversions and how products like Plasma One use this stack to offer USD₮ payments that feel instant.

Key Takeaways

ACH (Automated Clearing House) is batch-based and typically settles in 1-3 business days. Cross-border wires using SWIFT messaging and correspondent banking can take longer, depending on intermediaries and compliance checks.

Virtual accounts are digital sub-ledger identifiers linked to a master pooled account, enabling automated reconciliation and instant fund attribution without opening separate physical bank accounts per user.

Stablecoin infrastructure enables 24/7 settlement onchain, and when paired with instant fiat rails like RTP, the full on-ramp and off-ramp cycle can complete in seconds.

Bridge provides the virtual account and conversion infrastructure that powers products like Plasma One, converting between fiat and USD₮ programmatically.

How Traditional Banking Rails Move Money

ACH: Batch-Based Domestic Transfers

ACH, or Automated Clearing House, is a U.S. electronic network that banks use to process batch-based payments like direct deposits, payroll, and bill payments. Rather than clearing transactions individually, ACH groups them into batches that settle at specific windows during business days.

Standard ACH transfers typically settle in 1-3 business days, depending on bank processing. Same Day ACH can settle within hours if submitted before one of the three daily cutoff times. Because ACH only runs on business days, transactions initiated on a Friday evening may not settle until Monday or Tuesday.

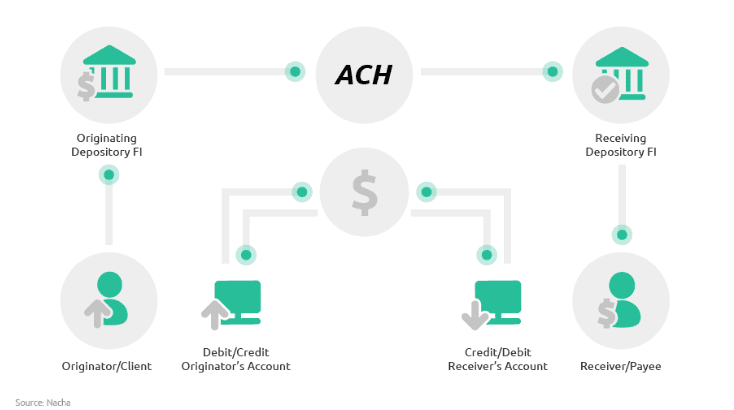

Overview of the ACH clearing process, highlighting the role of originating and receiving banks and the central ACH operator in batch-based settlement. Source: Vopay (Sourced from Nacha)

SWIFT and Correspondent Banking: Cross-Border Wires

SWIFT is a messaging network that banks use to send wire instructions internationally. It is not a settlement system itself; it tells banks what to do, and the banks move the money through their own correspondent relationships.

A correspondent bank is an intermediary that relays payments between institutions that don’t have a direct relationship. An international wire from the U.S. to Southeast Asia might route through two or three correspondent banks, each in a different time zone, each applying its own compliance checks and deducting fees from the principal.

This chain of intermediaries is why international wires typically take 1-5 business days and why senders often cannot predict exactly when funds will arrive or what the final amount will be after fees.

Real-Time Payment Rails

Newer payment rails like RTP (Real-Time Payments) in the U.S. and FPS (Faster Payments) in the UK settle individual transactions in real time with immediate finality, meaning the transfer is confirmed and cannot be reversed. These rails operate 24/7, removing the business-day constraint.

RTP changes the economics of on-ramp infrastructure significantly. When fiat deposits clear in real time, the bottleneck shifts from the banking leg to the conversion leg, which is where stablecoin infrastructure takes over.

Why Stablecoins Work as Settlement Layers

Stablecoins run on public blockchains that operate continuously. There are no batch windows, no business-day constraints, and no correspondent bank chains. A stablecoin transfer on a high-throughput network can confirm in seconds and finalize shortly after, at any time of day, any day of the year.

This 24/7 availability addresses the core limitation of traditional rails: time. When a business sends an international payment as a stablecoin transfer instead of a SWIFT wire, the settlement leg drops from days to seconds. The remaining friction is on the fiat side, getting money into and out of the stablecoin system, which is the problem that on-ramp and off-ramp infrastructure solves.

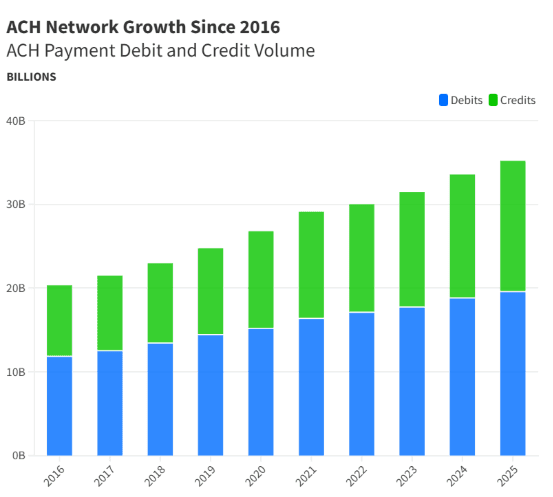

Bar chart illustrating the steady growth of ACH payment volumes from 2016 to 2025, with separate bars for debit and credit transactions, highlighting consistent year-over-year increases across both categories. Source: Nacha

Virtual Accounts: How Modern Fund Routing Works

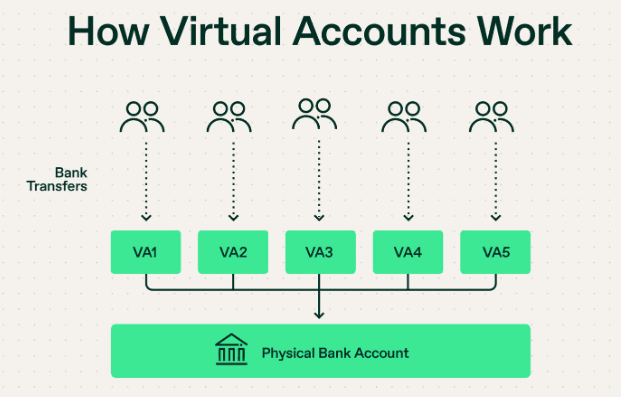

Virtual accounts solve a critical infrastructure problem: how to give thousands of users or transactions their own unique, routable identifiers without the overhead of opening a separate physical bank account for each one.

What Virtual Accounts Are

A virtual account is a digital identifier (often formatted as an account number or IBAN) that maps to an underlying physical bank account, sometimes called a master account, header account, or FBO (for benefit of) account. Multiple virtual accounts can map to a single physical account.

When money arrives at a virtual account, the banking system routes it to the underlying physical account, but the virtual layer tracks which sub-ledger the funds belong to. This enables automated reconciliation: the system knows instantly which user or transaction a deposit belongs to, without manual matching.

Virtual account identifiers map to a single pooled account, enabling automated reconciliation and user-level fund attribution. Source: Thunes

Why This Matters for On-Ramp Infrastructure

Without virtual accounts, an on-ramp provider would need to either open a separate bank account per user (operationally impractical at scale) or use a single shared account and reconcile deposits manually by matching amounts and reference codes (slow and error-prone).

Virtual accounts eliminate both problems. Each user gets a permanent, unique deposit identifier. When their deposit arrives, the system attributes it automatically and can trigger the next step in the pipeline, typically a stablecoin conversion, without human intervention.

Regulatory Considerations

Virtual accounts operate within existing banking regulations. In the EU, AMLR (Regulation (EU) 2024/1624) sets specific requirements for virtual IBANs, including identifying and verifying the user of a virtual IBAN and ensuring user identity information can be obtained within 5 working days when a virtual IBAN redirects payments to another institution. KYC (know your customer) verification applies at the virtual account level, meaning the provider must verify user identity before activating their account.

The Conversion Pipeline: Fiat to Stablecoin and Back

On-Ramp: Fiat to Stablecoin

The on-ramp process follows a consistent sequence regardless of provider:

The user initiates a fiat deposit (via ACH, wire, or RTP) to their assigned virtual account.

The deposit arrives and settles at the underlying physical bank account. The virtual account layer attributes it to the correct user.

A webhook (an automated message sent to the application’s backend when an event occurs) notifies the system that the deposit has arrived.

The system triggers an API call to convert the fiat to the configured stablecoin (e.g., USDC, USD₮).

The stablecoin is delivered to the destination wallet address.

The speed of the full flow depends on the fiat rail. If the deposit arrives via RTP, the entire sequence from bank transfer to stablecoin in wallet can complete in seconds. If it arrives via standard ACH, the fiat leg adds 1-3 business days, but the conversion and delivery happen immediately once settlement completes.

Off-Ramp: Stablecoin to Fiat

The off-ramp mirrors the on-ramp:

The user sends stablecoins to the provider’s designated address.

The provider confirms receipt and initiates a fiat payout instruction.

Fiat is sent to the user’s bank account via the appropriate rail (RTP for real-time, Same Day ACH for same-day, standard ACH or wire for others).

With RTP, fiat can arrive in real time. With Same Day ACH, it typically arrives within hours. The stablecoin leg is always fast; the variable is which fiat rail the user’s bank and region support.

Where Friction Still Exists

Stablecoin infrastructure removes friction from the settlement leg, but the fiat legs still have constraints worth understanding.

Batch Processing and Business-Day Limitations

ACH only runs on business days, and standard ACH batches have daily cutoff times. A deposit initiated late Friday may not settle until Monday or Tuesday. Same Day ACH helps but still has three daily submission windows.

Correspondent Banking Costs

For cross-border wires, every intermediary bank in the chain deducts fees from the principal, often without transparency. A $10,000 wire might arrive as $9,950 or $9,900 depending on the number of hops. The sender often has no way to predict the final amount. [NEEDS SOURCE: BIS data on pre-funding costs and correspondent banking inefficiencies]

Compliance and Risk Controls

Even when the technical infrastructure supports instant conversion, compliance reviews and risk controls can introduce delays. Providers may hold funds for additional verification on large deposits, new accounts, or transactions flagged by monitoring systems. These delays are a feature of responsible financial infrastructure, not a bug, but they mean "instant" is not always guaranteed.

Trapped Liquidity

The traditional correspondent banking model often requires companies to pre-fund foreign nostro accounts (bank accounts held at foreign banks to facilitate payments in that currency). This ties up working capital in accounts that exist solely to enable future transactions. The BIS has noted that this pre-funding requirement represents a significant opportunity cost for businesses engaged in global commerce. [NEEDS SOURCE LINK: BIS research on nostro account pre-funding]

How Bridge’s Infrastructure Handles This

Brand graphic featuring the Bridge logo. Source: Bridge

Bridge provides the stablecoin infrastructure that sits between traditional banking rails and blockchain networks. Rather than building each layer from scratch, applications integrate Bridge’s API to handle the full on-ramp and off-ramp pipeline.

Virtual Account Provisioning

Bridge assigns each customer permanent, local deposit details. For USD, this means a U.S. account number and routing number that supports both ACH push and wire transfers. When funds arrive at a virtual account, Bridge attributes them automatically and triggers the configured conversion flow.

Automated Conversion

Bridge’s conversion infrastructure operates continuously, matching the 24/7 nature of blockchain settlement. When a fiat deposit settles, Bridge converts it to the configured stablecoin and delivers it to the specified wallet address. Webhooks notify the application’s backend at each status change, so downstream actions (like crediting a user’s balance) can fire automatically without polling.

Conversion speed depends on the processing time of the inbound fiat rail. Deposits via Fedwire clear and settle with immediate finality. ACH deposits follow standard settlement timelines. The conversion and onchain delivery happen as soon as fiat settlement completes.

Bidirectional Flows

The architecture supports both directions. Incoming fiat deposits route to virtual accounts and trigger stablecoin conversions. Outgoing stablecoin redemptions convert and route to external bank accountsvia the appropriate rail. This bidirectional design means a single integration handles both on-ramp and off-ramp.

What This Looks Like in Practice

End-to-End Example: Cross-Border Payment

Consider a business in Florida paying a supplier in Singapore. Under the traditional model, the business initiates an international wire before the 5 PM cutoff. The wire routes through one or two correspondent banks, each deducting fees and running compliance checks. The supplier receives funds 1-5 business days later, minus intermediary fees, with limited visibility during transit.

Using stablecoin infrastructure: the business deposits USD into a virtual account via RTP. The deposit settles in real time. Bridge converts it to a stablecoin and delivers it onchain within seconds. The Singapore supplier receives the stablecoin in their wallet, confirms receipt, and initiates an off-ramp. If using an instant local rail, fiat lands in their bank account in real time.

The difference is settlement time (seconds vs. days), cost transparency (no hidden intermediary deductions), and availability (24/7 vs. business hours only).

Plasma One: Consumer & Business

For consumer and business products, this same pipeline runs in the background. In Plasma One, members top up their account from bank rails, hold USD₮, and send or spend globally. The on-ramp and off-ramp infrastructure is what makes the experience feel instant once fiat settlement completes. Members interact with a banking platform; the virtual accounts, stablecoin conversions, and blockchain settlement all happen behind the interface.

This is the design pattern that modern stablecoin infrastructure enables: the product is the payment experience, and the settlement layer is invisible.

Why Settlement Speed Matters for Businesses

Multi-day settlement creates tangible costs. Working capital gets trapped in transit, unavailable for operations or investment. Cash flow forecasting becomes harder when receivables are delayed by unpredictable timelines. Companies must maintain larger cash buffers to cover the uncertainty of when funds will actually arrive.

Stablecoin transfers settle in seconds to minutes at any time. Faster settlement can shorten pay cycles, reduce idle balances, and improve cash visibility when deposits and redemptions are automated. For businesses with global payment flows, this operational improvement is significant.

Disclaimer

This article is for educational and informational purposes only. It does not constitute, and should not be construed as, investment advice, financial advice, legal advice, tax advice, a solicitation, an offer, or a recommendation to buy, sell, or hold any digital asset or financial instrument. Stablecoin products and services may not be available or lawful in all jurisdictions. Settlement times described are illustrative and depend on specific providers, rails, and compliance requirements. Readers should conduct their own due diligence and consult qualified professionals before making any decisions.